Introduction:

Have you ever had a great idea, only to realize the money to make it happen just isn’t there? That’s exactly why choosing the right funding matters. The way you finance your goals can either smooth the path or turn it into a maze of stress, debt, or missed opportunities.

Take Mia, for example. She dreamed of opening a small café but started with a loan that had high interest and rigid repayment terms. Within months, the stress of meeting payments made her second-guess her business. Compare that to Raj, who combined his savings with a small investor contribution—he maintained control, reduced pressure, and could focus on growing his café.

Your My Funding Choice isn’t just a financial decision—it shapes how you approach your goals, manage risks, and even enjoy the journey. Picking wisely gives you freedom, confidence, and a clear path forward.

Table of Contents

Understanding Different Funding Options

When it comes to funding your goals, there isn’t a single “right” choice. Different options work for different people, depending on your goals, timeline, and risk tolerance. Let’s look at the main types:

Personal Savings

Starting with your own money is the simplest route. You don’t owe anyone, and you keep full control over your project. The main downside? Your resources might be limited, especially for bigger projects. It’s great for small ventures or testing ideas without pressure.

Loans

Loans give you access to capital you don’t currently have. Banks, credit unions, and online lenders are common sources. While loans let you expand your project faster, they come with interest and repayment obligations. It’s important to weigh the cost and flexibility carefully.

Investors & Equity Financing

If your goal has high growth potential, investors can help. Angel investors or venture capitalists provide funds in exchange for ownership stakes. The benefit is access to larger amounts of capital and sometimes guidance, but you give up some control over decisions.

Crowdfunding

Platforms like Kickstarter or GoFundMe let you raise money from many people, often in small amounts. Beyond funding, crowdfunding validates your idea and builds a community around it. However, it requires effort—creating engaging campaigns and actively promoting them.

Choosing the right option depends on your project size, risk tolerance, and personal preferences. Sometimes, a combination—like savings plus a small loan—gives the best balance.

Using Personal Savings: Pros and Cons

Using your own money to fund a project is often the first option people consider—and for good reason. It’s simple, straightforward, and low-risk in many ways. Since you’re not borrowing from a bank or giving away equity, there’s no interest, no repayment pressure, and no one else telling you how to run your project. That peace of mind alone can make a big difference.

Example: Imagine Lisa wants to start a small online store selling handmade candles. By using her savings, she can buy materials, set up her website, and test the market without worrying about monthly payments or investor expectations.

But personal savings do have limits. Not everyone has enough money to fund larger projects or cover unexpected costs. Overusing savings can also put your financial safety net at risk, leaving you stressed if things don’t go as planned.

Reflective Question: How much of your personal savings can you comfortably invest without putting your daily life or emergency funds in jeopardy?

Bottom line: Personal savings are great for small-to-medium projects and early testing, but bigger ambitions might require mixing in other funding options.

May be you like it:

How Long Does It Take to Learn Day Trading Effectively?

Boost Your Career with an Online Accounting Diploma

Smart Strategies for Generational Wealth Management

What Is a Smart Investment – Simple Guide for Beginners

Borrowing Smartly: Loans and Credit Options

Sometimes your savings just aren’t enough to bring a big idea to life. That’s where loans come in. Borrowing lets you access the capital you need now, but it’s important to approach it smartly.

You have several options: traditional bank loans, online lenders, and credit unions. Each has its pros and cons. Banks often offer lower interest rates but stricter approval requirements. Online lenders can be faster and more flexible but sometimes charge higher rates or hidden fees. Credit unions fall somewhere in between, usually with personalized service and competitive rates.

Interest rates, fees, and repayment terms are the most critical factors to watch. A low monthly payment might seem attractive, but if the term is long or there are hidden charges, it could end up costing more in the long run. Flexibility is key—look for loans that allow early repayment or temporary relief in case of unexpected challenges.

Mini Example: Jake needed funding to expand his mobile app startup. He compared a bank loan with a peer-to-peer online lender and chose a combination: a small bank loan for stability and a short-term online loan for immediate development costs. This mix gave him access to funds while keeping repayment manageable.

Reflective Question: If you take a loan, how much can you realistically repay each month without affecting your lifestyle or other responsibilities?

Bottom line: Loans are powerful tools, but only if you fully understand the costs, risks, and flexibility involved.

Investors & Equity Financing

If your project has big growth potential, sometimes personal savings or loans just won’t cut it. That’s where investors and equity financing come in. Angel investors, venture capitalists, or even strategic partners can provide the capital needed to scale quickly.

The big advantage? You get access to larger sums of money and, often, valuable guidance or connections. Investors bring experience, networks, and credibility that can help your project succeed faster.

But there’s a trade-off: sharing ownership and control. Giving away equity means you no longer have full say in decisions. Even small changes to your project might require investor approval, which can feel restrictive if your vision differs from theirs.

Mini Example: Emily wanted to launch a tech startup. She partnered with a small group of angel investors. They provided funds and mentoring, but she had to consult them before making big strategic moves. While the guidance was valuable, it required compromise on certain aspects of her original vision.

Reflective Question: Are you ready to share control of your project in exchange for funding, or do you prefer full independence even if growth is slower?

Bottom line: Investors can accelerate growth, but only if you’re comfortable balancing capital with shared decision-making.

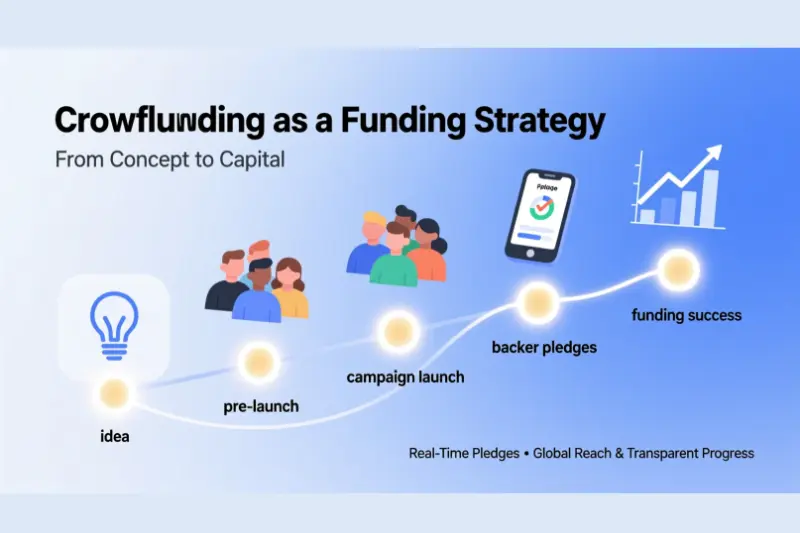

Crowdfunding as a Funding Strategy

Crowdfunding is more than just a way to raise money—it’s also a tool to test your idea and connect with your audience. Platforms like Kickstarter, Indiegogo, or GoFundMe let you pitch your project to a broad audience. If people are willing to support it financially, that’s a strong sign your idea resonates.

The biggest benefit? Beyond funding, you build a community around your project. Early supporters can become loyal customers, beta testers, or even advocates who help spread the word.

But crowdfunding isn’t passive. Successful campaigns require effort—compelling storytelling, clear visuals, regular updates, and active promotion. It’s not just asking for money; it’s marketing your idea and keeping backers engaged throughout the campaign.

Mini Example: Carlos wanted to launch a line of eco-friendly backpacks. He created a short video explaining the product, set clear funding goals, and shared updates throughout the campaign. Not only did he reach his funding target, but he also gained a dedicated group of customers before the product even hit the shelves.

Reflective Question: Could you commit the time and energy needed to run a campaign successfully, rather than just relying on the funds?

Bottom line: Crowdfunding can fund your project and validate your idea—but it requires dedication, creativity, and consistent effort.

How to Evaluate Your Funding Needs

Before committing to any funding option, it’s crucial to understand your needs clearly. Not all money is created equal, and picking the wrong source can slow you down or create unnecessary stress.

Start with goal clarity. What exactly are you trying to achieve? Is it a short-term project, like launching a small product, or a long-term venture, like building a startup? Knowing this will help you decide whether you need a small, low-risk source of funds or a larger, more flexible option.

Next, consider your timeline. If you need cash immediately, crowdfunding or loans might be faster than saving up or finding investors. If you have more time, personal savings or a gradual approach might be more comfortable.

Finally, think about your risk tolerance. Can you handle debt, or are you more comfortable funding your project with your own money? Are you okay sharing control with investors, or do you want full independence?

Mini Example: Nina wanted to start a boutique catering service. She mapped out her costs, timeline, and comfort with borrowing. She realized a small bank loan combined with her savings would cover startup costs without putting her personal finances at risk.

Reflective Question: If your first funding option doesn’t work out, do you have a backup plan that still aligns with your goals and comfort level?

Bottom line: Evaluate your funding needs carefully, match them to your resources, and choose an option that balances your goals, timeline, and risk.

May be you like it:

Free Trading Webinar: Learn Smart Market Strategies

Certificate in Business Management Online: Your Career Boost

Smart Generational Wealth Planning for Lasting Legacy

Top Personal Investment Company Tips for Smart Investors

Hybrid Funding Strategies

Sometimes, one funding source alone isn’t enough—or doesn’t feel comfortable. That’s where hybrid strategies come in, combining savings, loans, and small investments to balance risk, control, and access to capital.

The idea is simple: use your own money to cover initial costs, a small loan to manage larger expenses, and minor investments from friends, family, or angel investors to scale when needed. This approach spreads risk and gives you more flexibility without relying too heavily on one source.

Mini Example: Raj wanted to launch a specialty coffee shop. He used personal savings for equipment, a small bank loan to cover initial rent and salaries, and a minor angel investment for marketing and expansion. By mixing sources, he maintained control, minimized debt pressure, and had a safety net for unexpected costs.

Reflective Question: Could blending funding sources give you the flexibility and security that a single option alone might not?

Bottom line: Hybrid strategies aren’t just about money—they’re about smart planning. Combining funding sources can help you take bigger steps with less risk while keeping your project on track.

Common Pitfalls and Mistakes to Avoid

Even with careful planning, people often stumble when choosing how to fund their goals. Recognizing common mistakes can save you time, money, and stress.

Overleveraging Personal Savings or Debt

Putting too much of your savings or taking on excessive loans can leave you financially vulnerable. Unexpected costs or slow returns can quickly turn excitement into stress.

Chasing Trends or “Hot” Funding Options

Just because everyone is crowdfunding or taking investor money doesn’t mean it’s right for you. Following the crowd without evaluating your own goals can lead to poor decisions.

Ignoring Long-Term Implications

Every funding choice has consequences. Debt repayment, giving up equity, or losing flexibility can affect your next project or financial stability. Don’t focus only on short-term gains.

Tips to Safeguard Your Decisions:

- Compare all options side by side, including costs, risks, and flexibility.

- Keep an emergency fund separate from project funds.

- Ask reflective questions: “Can I realistically meet repayments?” or “Am I comfortable sharing control?”

- Consider a hybrid approach to balance risk and resources.

Mini Example: Karen took a high-interest loan for her small business without considering repayment pressure. Within months, she was juggling bills and losing focus on growth. Learning from that, she later combined savings with a smaller, low-interest loan, which gave her room to grow without stress.

Bottom line: Avoiding these pitfalls is just as important as choosing the right funding. Planning carefully and thinking ahead keeps your project on track and your stress levels manageable.

FAQs

What is “my funding choice” and why does it matter?

Your funding choice is the method you select to finance your goals—like using savings, loans, investors, or crowdfunding. It matters because the right choice affects your control, risk, and how smoothly your project runs. Picking poorly can cost time, money, and stress.

How do I know which funding option suits me best?

Start by clarifying your goal, timeline, and risk comfort. Are you okay giving up equity, or do you prefer full control? Compare costs, effort, and long-term impact. Sometimes a mix of options—like savings plus a small loan—works best.

Are personal savings a good way to fund a project?

Yes, especially for small or low-risk projects. Savings mean no interest or debt, and you keep full control. But the downside is limited funds, so it may not cover bigger goals. Always protect your emergency savings first.

When should I consider investors or equity funding?

If your project has high growth potential and needs significant capital, investors can help. Just remember, you’re sharing ownership, so decisions aren’t entirely yours. Only choose investors whose vision aligns with yours.

Can crowdfunding really work for serious projects?

Absolutely, but it requires effort. Crowdfunding helps raise money and test market interest at the same time. Successful campaigns need clear storytelling, engaging updates, and active promotion. Think of it as funding plus marketing rolled into one.

Making Your Funding Choice with Confidence

Choosing how to fund your goals can feel overwhelming, but it doesn’t have to be. The key is clarity, reflection, and practical planning. When you understand your options, assess your needs, and weigh risks, you can make a decision that feels right for you.

Ask yourself questions like:

- “Which funding option aligns best with my goals and timeline?”

- “How much risk am I comfortable taking?”

- “Am I okay sharing control or taking on debt if it helps me grow?”

Taking a moment to reflect can prevent costly mistakes and give you peace of mind.

Mini Insight: Many successful entrepreneurs use a mix of strategies, adjusting as their project evolves. Funding isn’t a one-time choice—it’s a process. Your first decision doesn’t lock you in forever.

The most important step? Take action with confidence. Whether it’s using your savings, applying for a loan, pitching to investors, or launching a crowdfunding campaign, what matters is moving forward informed and prepared. Every small, thoughtful step brings you closer to achieving your goals.

Bottom line: Your funding choice shapes not only how your project starts but also how it grows. Make it wisely, stay flexible, and trust yourself.

May be you like it:

Stock Market for Beginners PDF – Your Simple Starter Guide

Top MBA Certificate Programs Online for Career Growth