Introduction:

Imagine finding your dream home-the perfect kitchen, a cozy living room, and a balcony with a view. Exciting, right? But then comes the reality check: the home loan. While the property price grabs attention, it’s the home loan interest rate that silently decides how heavy-or light-your monthly EMIs will be.

Even a small difference in interest rates can cost you lakhs over a 15–20 year loan period. For example, on a ₹50 lakh loan, a 1% higher interest rate can increase your monthly EMI by several thousand rupees and add years of extra payments. That’s not a small detail-it’s a game-changer for your budget and long-term financial comfort.

Understanding interest rates isn’t just for finance buffs. Whether you’re a first-time buyer or planning to upgrade your home, knowing how rates work and how they affect your repayment can save you serious money, prevent stress, and even guide your choice of lender. In short, interest rates matter more than you might think-and a little knowledge now can pay off handsomely later.

Table of Contents

What Are Home Loan Interest Rates?

At its core, a home loan interest rate is the cost you pay to a bank or lender for borrowing money to buy or build a house. Think of it as the “rent” you pay for using someone else’s money. The higher the rate, the more you pay over time, even if the loan amount stays the same.

To understand it better, let’s break down a home loan:

- Principal: This is the actual amount you borrow. For example, if your home costs ₹50 lakh and you take a loan for the full amount, ₹50 lakh is your principal.

- Interest: This is the extra money the bank charges for lending you the principal. The rate determines how much this will be.

- EMI (Equated Monthly Installment): Your monthly payment combines both principal and interest. Part of the EMI goes toward reducing the loan, while the rest pays the interest.

Here’s a simple observation from real life: in the early years of a loan, most of your EMI goes toward interest, and only a small portion reduces your principal. That’s why even a 0.5% difference in the interest rate can significantly affect your monthly budget and total repayment over 15–20 years.

So, while the property price may grab headlines, the home loan interest rate quietly decides how affordable your dream home really is. Understanding this is the first step to making smarter financial decisions.

Current Trends in Home Loan Interest Rates

Home loan interest rates aren’t static-they move up and down like the tide, influenced by bigger economic currents. Over the past few years, many borrowers have noticed a mix of surprises and opportunities. Rates dipped during economic slowdowns to encourage borrowing, and they rose when inflation spiked or central banks tightened policies.

Right now, the market shows a cautious balance. Many banks offer slightly higher rates than a year ago, reflecting inflation pressures and adjustments in central bank benchmarks. At the same time, competition among lenders keeps options open, so borrowers can still find attractive deals if they compare carefully.

What Drives These Changes?

- Central Bank Policies: When the Reserve Bank of India (or your local central bank) changes its repo rate, banks often adjust home loan interest rates in response. Lower repo rates can make loans cheaper; higher rates push EMIs up.

- Inflation: Rising inflation reduces the purchasing power of money, prompting lenders to raise rates to maintain returns.

- Economic Conditions: Slow economic growth may encourage banks to lower rates to attract borrowers, while strong growth periods may see rates rise.

A real-life takeaway: if you’re planning to take a loan, tracking these trends-even casually-can help you time your application better. For instance, a borrower I advised recently waited a few months for a minor dip in rates and ended up saving over ₹50,000 in interest in the first year alone.

May be you like it:

Top 10 Best Trading YouTube Channels to Follow in 2025

Funding an LLC: Easy Ways to Get Startup Money

Family Wealth Strategy – Build and Protect Your Legacy

Invest Wisely: Smart Tips for Growing Your Money

Fixed vs Floating Home Loan Interest Rates

One of the first big choices every homebuyer faces is whether to go with a fixed or floating interest rate. Understanding the difference can save you stress-and a lot of money-over the life of your loan.

Fixed Interest Rates

A fixed rate stays the same for a specified period, usually 3–5 years or even the entire loan tenure. Your EMI remains predictable, which makes budgeting simple.

Pros:

- Stability: Your EMI won’t change even if market rates rise.

- Peace of mind: No surprises, perfect for borrowers with strict monthly budgets.

Cons:

- Slightly higher initial rates compared to floating loans.

- You might miss out on lower rates if the market dips.

Example: If you borrow ₹50 lakh at a fixed 7% rate for 20 years, your EMI will remain the same every month-around ₹38,800-even if the bank reduces rates later.

Floating Interest Rates

A floating rate changes with market conditions, usually linked to the central bank’s benchmark rates. Your EMI can increase or decrease depending on these movements.

Pros:

- Potentially lower rates over time, saving you money in interest.

- More flexibility if you plan to prepay or shorten your tenure.

Cons:

- EMI uncertainty: Payments can rise unexpectedly, which can stress your budget.

- Requires careful planning and monitoring.

Example: Borrow ₹50 lakh at a floating rate of 6.5%. If the rate drops to 6% after a year, your EMI reduces to about ₹37,400. But if the rate rises to 7%, your EMI jumps to roughly ₹39,200.

When to Choose Which

Ask yourself a few questions:

- Do you prefer predictable payments even if it costs slightly more? → Fixed might suit you.

- Can you handle fluctuating EMIs and want to save interest if rates fall? → Floating is worth considering.

Many borrowers opt for a hybrid approach: fix the rate for the initial years for stability, then switch to floating to benefit from potential rate drops. This strategy balances security and savings.

Factors That Affect Home Loan Interest Rates

Not all home loans are created equal. Even for the same property, two borrowers might get different interest rates. Why? Several factors influence what the bank ultimately offers. Understanding these can help you secure a lower rate and save money over the long term.

Credit Score

Your credit score is like a report card for your financial discipline. Banks see a high score as a sign that you’re responsible and less likely to default.

Tip: A score above 750 often qualifies for better rates. If yours is lower, take a few months to clear debts, pay bills on time, and reduce credit card utilization before applying.

Real-life observation: I’ve seen borrowers with similar incomes get a 0.5–1% lower rate just because they had a better credit score. That can save lakhs over a 20-year loan.

Loan Amount and Tenure

The size of the loan and how long you plan to repay it also matter. Larger loans or longer tenures sometimes come with slightly higher rates because they carry more risk for the lender.

Tip: Consider a tenure that balances affordable EMIs and total interest paid. Even shortening the loan by 5 years can reduce your interest burden significantly.

Property Type

Not all properties are treated the same by lenders. Rates may differ for:

- Under-construction properties (slightly higher risk)

- Resale homes

- Self-built houses

Observation: Banks often charge a marginally higher rate for under-construction homes because completion risks exist.

Lender Policies

Each bank or housing finance company has its own internal criteria. Some may offer special discounts for salaried employees, women borrowers, or customers with existing accounts.

Tip: Don’t assume one bank’s rate is fixed. Compare multiple lenders and ask for personalized quotes. A 0.25–0.5% difference can save you thousands per month.

Market and Economic Conditions

External factors like inflation, repo rates, and the overall economy also influence rates. Even if your profile is perfect, interest rates can fluctuate slightly with market conditions.

Key Takeaway: By understanding these factors, you can plan ahead. Improving your credit score, choosing the right tenure, and shopping around for lenders are small steps that create big savings over the life of your home loan.

How Home Loan Interest Rates Impact Your EMI and Total Repayment

Here’s where the numbers start to hit home-literally. Even small changes in home loan interest rates can significantly affect your and the total amount you repay over the loan tenure.

Why It Matters

The EMI (Equated Monthly Installment) is calculated based on the loan principal, interest rate, and tenure. A slightly higher interest rate doesn’t just increase your monthly payment-it also adds up over 15–20 years, sometimes costing you lakhs extra.

Real-Life Example

Let’s say you take a home loan of ₹50 lakh for 20 years.

- At a 6.5% interest rate, your EMI would be roughly ₹38,700, and the total interest paid over 20 years would be about ₹43.7 lakh.

- If the rate rises to 7%, the EMI jumps to ₹40,900, and total interest increases to approximately ₹48 lakh.

That’s an extra ₹2,200 per month and over ₹4 lakh in total interest, just because of a 0.5% difference in interest rate.

Key Takeaways

- Small rate differences matter: Even a fraction of a percent can affect your finances significantly.

- Longer tenure magnifies the impact: The longer you take to repay, the more the interest difference adds up.

- EMI planning is crucial: Always ensure your budget can handle a slight increase in rates, especially if you opt for a floating interest rate.

Reflect for a moment: if your monthly EMI increased by ₹2,000–3,000, could you comfortably adjust your budget? Thinking about this upfront can prevent stress years down the line.

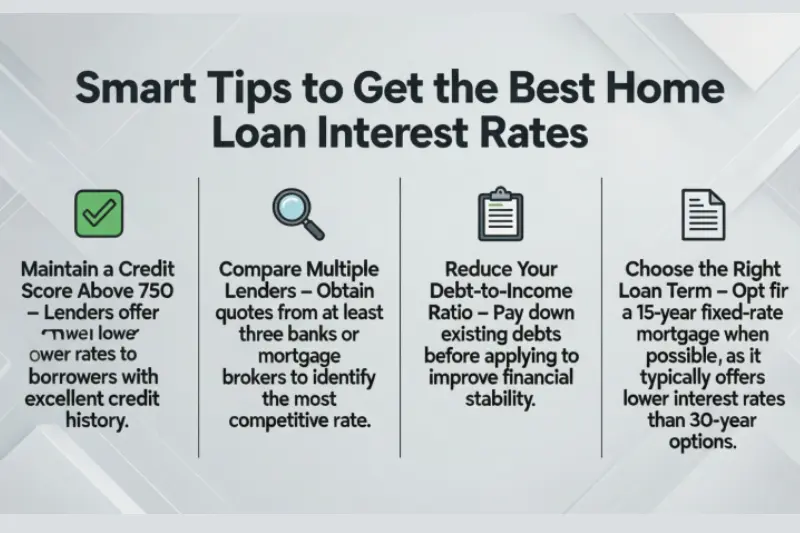

Smart Tips to Get the Best Home Loan Interest Rates

Securing a home loan is one thing, but getting the best possible interest rate is what can save you lakhs over time. Here are actionable tips that have worked for real borrowers:

Improve Your Credit Score

Your credit score is one of the biggest factors lenders consider. A higher score signals reliability, making banks more willing to offer lower rates.

Actionable tip: Pay off outstanding debts, avoid missing any bill payments, and keep credit card balances low before applying. Even a 50-point improvement can reduce your rate by 0.25–0.5%.

Compare Multiple Lenders

Don’t settle for the first offer. Banks and housing finance companies often have different rates, processing fees, and special schemes.

Practical approach: Use online comparison tools or request personalized quotes. A small difference in rate could save thousands per month on EMIs.

Negotiate Confidently

Many borrowers assume rates are fixed. In reality, lenders often have some flexibility, especially if you have a stable income and a good credit history.

Tip: Ask your bank or HFC if they can match or beat competitors’ offers. Even a 0.1–0.2% reduction can make a difference over a 20-year loan.

Consider Balance Transfers

Already paying a higher interest rate? A balance transfer to another lender offering lower rates can reduce your monthly EMI and total interest.

Observation: One of my clients saved over ₹30,000 annually by transferring her loan to a lender with a 0.5% lower rate. Just factor in processing charges before making the move.

Optimize Loan Tenure

While longer tenures reduce monthly EMIs, they also increase total interest paid. Shorter tenures often get lower rates and save money in the long run.

Tip: If your income allows, slightly higher EMIs with a shorter tenure can dramatically reduce the total interest. For example, reducing a 20-year loan to 15 years can cut interest payments by 20–25%.

Common Borrower Mistakes

Even experienced homebuyers can slip up when it comes to home loan interest rates. These mistakes might seem small at first, but over 15–20 years, they can cost you dearly. Recognizing them early can save both money and stress.

Ignoring Floating Rate Changes

Many borrowers choose a floating rate and then forget it exists. Rates can rise unexpectedly, increasing your EMI without warning.

Tip: Keep an eye on market trends and central bank decisions. Being proactive lets you plan your budget or even consider refinancing if rates rise significantly.

Choosing an Overly Long Tenure

Longer tenures lower your monthly EMI, which feels attractive initially. But more time means more interest paid overall.

Observation: I’ve seen borrowers stretch a 20-year loan to 25 years to reduce EMI. The short-term relief often leads to paying lakhs extra in interest.

Tip: Balance affordability with total repayment. Slightly higher EMIs for a shorter loan can save a substantial amount over time.

Overlooking Fine Print

Many borrowers focus on the headline interest rate but ignore clauses like processing fees, prepayment penalties, or rate reset periods.

Tip: Read your loan agreement carefully. Ask questions if anything isn’t clear. Transparency now prevents surprises later.

Not Considering Refinancing

Even if you’re already paying a home loan, interest rates can drop over time. Not exploring a balance transfer or refinancing opportunity can mean leaving money on the table.

Tip: Periodically review your loan. If a better deal exists, moving your loan could reduce EMIs and total interest significantly.

Reflective question for readers: Could a few simple checks today-like reviewing your tenure or monitoring rates-save you tens of thousands in the future? Often, the smartest decisions are the ones that seem small at the moment.

Tools to Help Borrowers: EMI Calculators & Simulations

When it comes to home loans, numbers matter-and small changes can have big consequences. That’s where EMI calculators and simulations become your best friends. They take the guesswork out of planning and give you a clear picture of what to expect.

How EMI Calculators Work

An EMI calculator allows you to input:

- Loan amount

- Interest rate

- Tenure

The tool instantly shows your monthly EMI and total interest payable. It’s simple, fast, and far more reliable than trying to estimate on your own.

Real-life tip: I often tell borrowers to play with these numbers before even visiting a bank. It helps them understand what is truly affordable versus what feels affordable at first glance.

Experiment with Different Scenarios

EMI calculators aren’t just about one fixed scenario. You can:

- Adjust the interest rate to see how small changes impact EMIs

- Change the tenure to explore how a slightly shorter or longer loan affects total repayment

- Compare fixed vs floating rates to visualize potential savings or risks

Example: For a ₹50 lakh loan:

- At 6.5% for 20 years → EMI ≈ ₹38,700

- At 7% for 20 years → EMI ≈ ₹40,900

- At 6.5% for 15 years → EMI ≈ ₹43,300 (but total interest paid drops significantly)

Playing with these scenarios gives a real sense of control. Instead of being surprised by rising EMIs, you can plan, budget, and even decide if refinancing or switching lenders makes sense.

Why Borrowers Should Use Them

Many people skip this step and rely on the bank’s quoted EMI. That’s risky. Using calculators:

- Gives clarity on affordability

- Helps you plan for rate fluctuations

- Encourages smarter decisions about tenure, prepayments, and loan type

Reflective question: Could spending 10 minutes experimenting with your EMI today prevent years of financial stress tomorrow? The answer is often yes.

May be you like it:

Top Finance Webinars to Boost Your Money Skills

My Funding Choice: Find the Best Way to Finance Your Goals

Wealth and Success – Habits That Transform Your Future

Invest Criteria: How to Choose Smart Investments

FAQs

What exactly are home loan interest rates?

They are the cost charged by a bank or lender for borrowing money to buy or build a home, expressed as a percentage of the loan amount.

Should I choose a fixed or floating interest rate?

Fixed rates give predictable EMIs and stability, while floating rates can save money if market rates fall. Your choice depends on your budget and risk comfort.

How can I get the lowest home loan interest rate?

Improve your credit score, compare multiple lenders, negotiate, and consider balance transfers or shorter loan tenures.

Do small changes in interest rates really matter?

Absolutely. Even a 0.5% difference can increase EMIs by thousands per month and add lakhs to total repayment over 15–20 years.

Are low interest rates always the best option?

Not always. Some low-rate offers are introductory, come with hidden fees, or have strict conditions. Focus on transparency and long-term affordability, not just the advertised rate.

What Affects Your Home Loan Interest Rate?

Your credit score, loan amount, tenure, property type, and the lender’s policies all influence the rate you’re offered. Market conditions like inflation and central bank decisions also play a role.

What Are the Cheapest Home Loan Rates in 2026?

The lowest rates vary by lender and borrower profile, but typically banks offering competitive schemes, good credit incentives, or special promotions provide rates around 6–7%. Always compare before deciding.

Fixed vs Variable: Which Offers the Better Value?

Fixed rates provide stability and predictable EMIs, while variable (floating) rates can save money if interest rates drop. The best choice depends on your risk tolerance and financial flexibility.

Why Work with The Finance Nest?

The Finance Nest helps you compare lenders, understand rates, and choose the right home loan based on your budget and goals. Their guidance can save time, money, and stress.

Conclusion

Home loan interest rates might seem like just another number on a bank document, but they quietly shape your financial life for decades. A small difference in rates can change your EMI, total repayment, and even your comfort level with your monthly budget.

The key takeaway? Awareness and planning pay off. Understanding fixed vs floating rates, improving your credit score, comparing lenders, and using tools like EMI calculators can make a real difference. Even small actions-like negotiating a slightly lower rate or choosing the right tenure-can save you lakhs over the life of your loan.

Remember, a home loan should support your dream, not stress your life. Ask questions, do your research, and make choices that fit your financial reality. When it comes to home loan interest rates, being proactive now means financial peace and confidence for years to come.

May be you like it:

Best Day Trading Setup – Simple Strategies That Work

Business Finance Definition Made Easy for Understanding Info