Introduction

Buying a car is exciting – the smell of a new interior, the thrill of hitting the road in your own ride. But let’s be real: the paperwork, loans, and insurance can quickly turn that excitement into stress. Have you ever sat down to figure out your monthly payments, only to realize the numbers don’t add up once insurance is factored in? You’re not alone.

Understanding how to finance cars and insurance together isn’t just about saving money – it’s about making a choice you’ll feel confident about for years. When you look at loans and insurance as connected pieces rather than separate headaches, you can avoid surprises, hidden costs, and buyer’s remorse.

In this guide, we’ll walk through the essentials: from choosing the right loan to picking the right coverage, budgeting smartly, and spotting 2026 trends that can affect your decision. By the end, you’ll know exactly how to make a car purchase that protects both your wallet and your peace of mind.

Table of Contents

Understanding Car Financing

When most people hear “car financing,” their minds jump straight to loans – and for good reason. Financing a car is essentially borrowing money to buy a vehicle, then paying it back in monthly installments. But there’s more to it than just signing a contract and driving off the lot. Understanding the basics can save you serious money and stress.

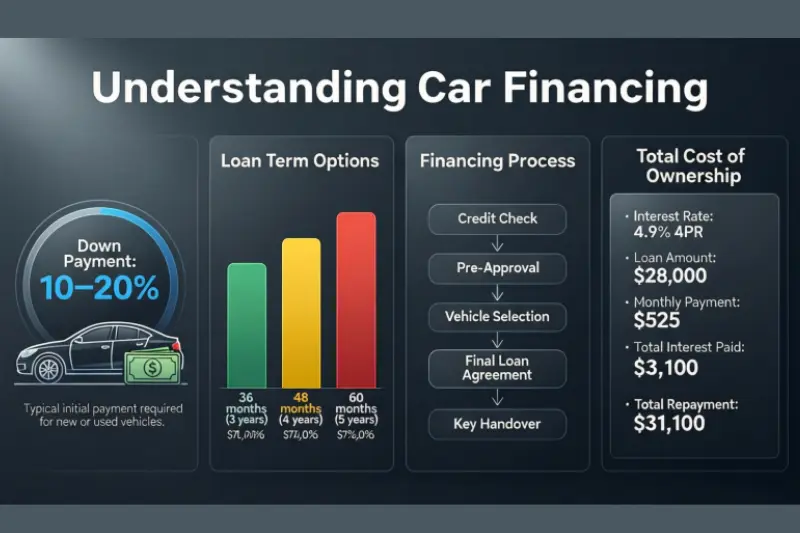

Basics of Auto Loans

An auto loan is a legal agreement between you and a lender. You borrow a set amount – usually the car’s price minus any down payment – and agree to repay it over a specific term, often 36 to 72 months. While the idea seems simple, the fine print matters. Early repayment fees, pre-approval rates, and hidden charges can all affect the overall cost.

Interest Rates and How They Affect Total Cost

Interest is where many people get surprised. Even a seemingly small difference in rates can add up over time. For example, a $25,000 loan at 3% interest over five years costs roughly $2,000 in interest, while the same loan at 8% jumps to almost $5,500. That’s over $3,000 more for the exact same car – just because of the rate.

Your credit score, the lender, and even the type of vehicle (new vs. used) can influence the rate. That’s why it’s worth shopping around, comparing offers, and understanding how different terms impact your total payment.

Difference Between Buying and Leasing

Leasing is often confused with financing. Here’s the distinction: when you finance (or buy) a car, you’re building ownership. Once the loan is paid off, the car is yours. Leasing, on the other hand, is essentially a long-term rental. Your monthly payments may be lower, but at the end of the lease, you either return the car or pay a residual value to own it.

If you drive a lot, like to personalize your ride, or plan to keep the car for several years, financing is usually the smarter option. Leasing might be tempting for short-term convenience, but it rarely offers the same long-term financial advantage.

May be you like it:

Top 10 Best Trading YouTube Channels to Follow in 2025

Funding an LLC: Easy Ways to Get Startup Money

Family Wealth Strategy – Build and Protect Your Legacy

Invest Wisely: Smart Tips for Growing Your Money

Choosing the Right Loan Option

Once you understand how car financing works, the next step is picking the loan that fits your lifestyle and budget. Not all loans are created equal, and a small difference in terms or rates can mean big savings – or unexpected stress.

Loan Terms: Short vs. Long

Loan terms usually range from 36 to 72 months. Shorter loans generally have higher monthly payments but cost less in interest overall. Longer loans lower your monthly payments but often increase the total interest you pay over time.

For example, a 5-year loan might feel easier on your wallet month-to-month, but you could end up paying hundreds or even thousands more in interest than a 3-year loan. It’s a trade-off between immediate comfort and long-term savings.

How Credit Score Impacts Rates

Your credit score is like a financial report card – lenders use it to decide how risky it is to loan you money. A higher score usually means lower interest rates, while a lower score can result in higher rates or even loan denial.

Don’t worry if your score isn’t perfect. Checking your credit report, paying down small debts, and pre-qualifying for loans can help you secure a better rate. Even a 1–2% difference in interest can save you hundreds over the life of the loan.

Tips for Comparing Lenders

When shopping for a car loan, don’t just look at the monthly payment. Compare:

- Total interest over the life of the loan

- Fees (origination, late payment, prepayment penalties)

- Flexibility for early repayment

It’s also wise to check rates from multiple sources: banks, credit unions, online lenders, and dealership financing. Sometimes the dealer’s offer is convenient, but not always the most cost-effective.

Mini tip: Pre-qualifying with a lender can give you a clear idea of what to expect without hurting your credit score – and it strengthens your negotiation power at the dealership.

Car Insurance Basics

Once you’ve figured out your loan, the next piece of the puzzle is insurance. Think of it as protecting not just your car, but your wallet and peace of mind. Many people underestimate how much insurance impacts the overall cost of owning a financed car, so it’s worth getting it right from the start.

Types of Coverage

There are three main types of car insurance coverage you’ll want to know:

- Liability Coverage – This covers damage or injuries you cause to others in an accident. It’s usually the minimum required by law, but it won’t pay for your own car if something happens.

- Collision Coverage – This pays for damage to your car if you’re in an accident, no matter who’s at fault. For financed cars, lenders often require this because they want their investment protected.

- Comprehensive Coverage – This covers non-collision events like theft, fire, vandalism, or natural disasters. If you only have liability or collision, you could still be on the hook for full repair or replacement costs.

Mini example: Imagine you just bought a new car with a loan, and someone hits it in a parking lot. Without collision or comprehensive coverage, you’d still owe the lender the full loan amount – even though your car is damaged. Ouch.

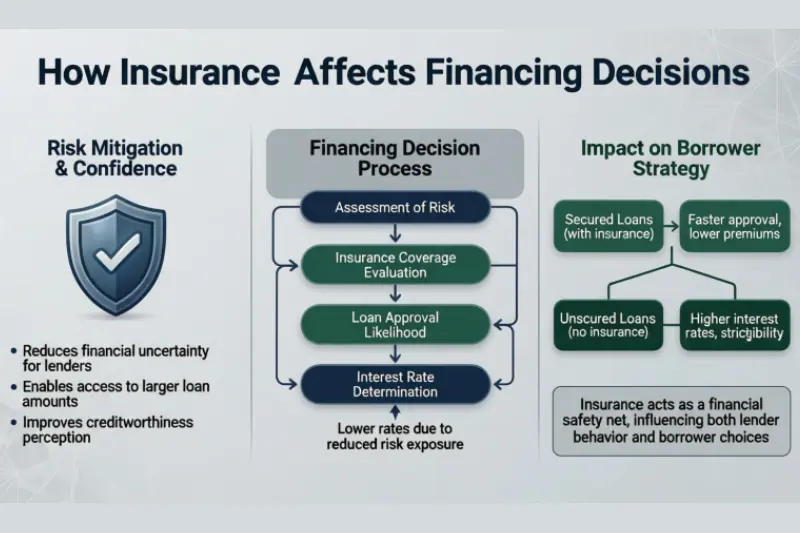

Why Insurance is Mandatory for Financed Cars

Here’s the deal: if you finance a car, the lender technically owns it until the loan is paid off. That’s why lenders almost always require full coverage – at least collision and comprehensive.

Not having adequate insurance isn’t just risky; it could also violate your loan agreement, which might lead to penalties or even repossession.

Insurance might feel like an extra monthly expense, but when combined with smart financing, it ensures that your investment is protected and your monthly budgeting stays predictable.

How Insurance Affects Financing Decisions

Many people treat car financing and insurance as separate steps, but in reality, they’re closely linked. Your insurance premium directly affects how much you can comfortably afford each month, and overlooking it can turn a seemingly manageable loan into a financial headache.

Premium Impact on Monthly Budget

Think of it this way: your monthly loan payment is only part of the total cost of owning a financed car. Insurance premiums can add hundreds of dollars to your monthly expenses. A car with a $400 loan payment but a $150 insurance premium actually costs $550 per month – and that’s before gas, maintenance, or unexpected repairs.

Budgeting only for the loan can leave you stretched thin, which is why it’s smart to include insurance in your planning from the start.

Hidden Costs if Coverage is Inadequate

Skimping on insurance to save money upfront can backfire. If your coverage is too low, you might face:

- High out-of-pocket repair costs

- Penalties from your lender for failing to meet coverage requirements

- Financial stress if you’re in an accident or your car is stolen

Mini example: A friend of mine financed a car with minimal coverage to save $50 per month. Two months later, someone backed into their parked car. The repair cost was $3,000 – more than the total savings they had hoped for.

Real-Life Examples of Underinsurance

Underinsurance is surprisingly common. For instance:

- Someone buys a used car with only liability coverage and gets rear-ended. They’re left paying thousands for repairs while still owing the full loan amount.

- Another person goes for the cheapest comprehensive plan, not realizing it excludes natural disasters. A storm destroys the car, and the payout doesn’t cover the remaining loan.

These examples show why it’s important to think about finance cars and insurance together, not as separate line items. The right coverage keeps your finances predictable and protects your investment in the long run.

Bundling Finance and Insurance

One strategy that’s gaining popularity in 2026 is bundling your car loan and insurance together. At first, it might sound like a marketing gimmick, but when done right, it can actually simplify the process and sometimes save you money.

Dealership and Lender Packages

Many dealerships and lenders now offer bundled options where financing and insurance are combined into a single monthly payment. This can make the paperwork simpler – instead of dealing with separate bills and approvals, you get everything sorted at once. Some packages even offer slightly lower rates on either the loan or insurance as an incentive.

Pros and Cons of Bundled Options

| Pros | Cons: |

| Convenience: One-stop solution for both financing and insurance | Limited flexibility: You may not be able to shop around for the best insurance deal |

| Potential savings: Some lenders offer discounted rates | Hidden fees: Bundled packages sometimes include charges that aren’t obvious upfront |

| Simplified budgeting: One payment to track | Less control: You may end up paying for coverage you don’t really need |

How to Read the Fine Print

Before jumping on a bundled package, read the agreement carefully. Look out for:

- Prepayment penalties on the loan

- Minimum coverage requirements or policy exclusions

- Automatic renewals or additional fees

Mini insight: A bundle can be great if it genuinely saves money and time, but don’t let convenience override your need for the right coverage or best loan terms. Think of it as an option to consider, not a default choice.

By understanding bundles, you’re taking another step toward smartly managing finance cars and insurance – combining practicality with protection.

Budgeting for Total Ownership Cost

Buying a car isn’t just about the sticker price or monthly loan payment. If you really want to make a smart decision, you need to look at the total cost of ownership – everything that comes with driving and maintaining the vehicle.

Loan Payment + Insurance + Maintenance

Your total monthly cost isn’t just your loan. Think of it as three main components:

- Loan Payment – The amount you agreed to pay the lender each month.

- Insurance Premium – Coverage required for financed cars, including liability, collision, and comprehensive.

- Maintenance & Repairs – Oil changes, tires, unexpected repairs, or even seasonal check-ups.

Ignoring even one of these can make your budget feel tighter than expected. For example, a $400 loan payment might seem affordable – but once you add $150 insurance and $50 for routine maintenance, you’re really spending $600 a month.

Calculating Total Monthly Cost

A simple approach is to list all expected costs and add a small buffer (say, 10–15%) for unexpected expenses. Here’s a quick example:

| Expense | Monthly Cost |

|---|---|

| Loan Payment | $400 |

| Insurance | $150 |

| Maintenance | $50 |

| Fuel & Misc | $100 |

| Total | $700 |

This gives you a clear picture of what you’ll actually pay each month, so there are no surprises when bills arrive.

Tips to Avoid Financial Stress

- Plan for unexpected costs: Keep an emergency fund for repairs or insurance deductibles.

- Choose a loan term wisely: Shorter loans save interest, but ensure monthly payments fit comfortably into your budget.

- Shop around for insurance: Even small differences in premiums can add up to hundreds of dollars per year.

- Track spending: Use apps or spreadsheets to monitor car-related expenses – knowledge is power.

By taking a realistic look at the finance cars and insurance combination, you can enjoy your vehicle without financial anxiety. After all, the goal is to drive happy, not stressed.

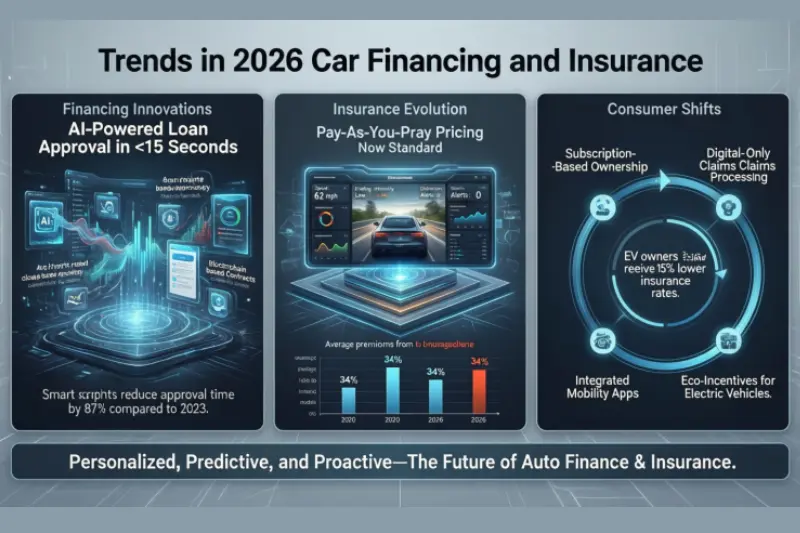

Trends in 2026 Car Financing and Insurance

The car market in 2026 is evolving fast, and staying on top of trends can give you an edge when financing and insuring your vehicle. From digital tools to eco-friendly incentives, understanding these shifts can save you money and simplify the process.

Digital Tools for Loan Approval

Gone are the days of waiting in long dealership lines and filling out stacks of paperwork. Today, many lenders offer instant online pre-approval. You can check rates, compare offers, and even lock in a loan before stepping foot in a dealership – all without affecting your credit score.

Mini insight: Pre-approval not only gives you confidence about what you can afford, but it also strengthens your negotiation power when choosing your car.

Usage-Based Insurance

Insurance companies are increasingly offering plans that charge based on how much – and how safely – you drive. Using telematics devices or smartphone apps, insurers can track driving behavior and reward careful drivers with lower premiums.

If you’re a low-mileage driver or someone who rarely speeds, this could cut hundreds off your annual insurance cost. It’s a perfect example of how 2026 trends are making finance cars and insurance more personalized and cost-effective.

EV Incentives and Their Impact

Electric vehicles (EVs) are no longer niche – and they come with perks. Governments and manufacturers offer tax incentives, rebates, and lower insurance premiums for EV owners. These incentives can make financing an EV more attractive, while also affecting insurance options and costs.

Example: A $40,000 EV with a $7,500 federal rebate effectively reduces your loan amount to $32,500, which can also lower insurance premiums since some insurers offer discounts for EVs with advanced safety features.

Keeping up with these trends ensures you’re not overpaying on loans or insurance and can help you make smarter, more informed decisions for 2026 and beyond.

May be you like it:

Top Finance Webinars to Boost Your Money Skills

My Funding Choice: Find the Best Way to Finance Your Goals

Wealth and Success – Habits That Transform Your Future

Invest Criteria: How to Choose Smart Investments

Practical Tips for First-Time Buyers

Buying your first car can feel like stepping into a maze – there are loans, insurance policies, and endless options. The good news? A little preparation goes a long way, and understanding how to finance cars and insurance together can make the process much smoother.

Preparing Documents

Before visiting a dealership or applying for a loan, make sure you have all necessary paperwork ready:

- Proof of income (pay stubs or bank statements)

- Credit report or history

- ID and residency documents

- Insurance information (if pre-approved or exploring policies)

Having these ready can speed up approvals and show lenders that you’re organized and serious – which can sometimes help secure better rates.

Negotiation Tips

Negotiation isn’t just about haggling over the car price. You can also:

- Compare multiple loan offers and mention pre-approvals

- Ask if there are any bundled finance + insurance discounts

- Don’t be afraid to walk away if the deal doesn’t feel right

A confident, informed approach often leads to better deals and prevents overpaying. Remember, dealerships expect negotiation – it’s part of the game.

Checking Loan and Insurance Options Online

The internet is your best friend. Use online tools to:

- Compare interest rates across banks, credit unions, and lenders

- Get insurance quotes instantly and see what coverage fits your budget

- Explore digital pre-approval to know your limits before you shop

Mini insight: Doing this homework online not only saves time, it gives you leverage during negotiations. You’ll walk into the dealership knowing exactly what you can afford and what’s fair.

With a bit of preparation, first-time buyers can confidently navigate both finance cars and insurance without feeling overwhelmed – and avoid common pitfalls that trip up many newbies.

Conclusion:

Buying a car in 2026 doesn’t have to feel like navigating a maze blindfolded. When you understand how to finance cars and insurance together, you’re not just signing paperwork – you’re making a decision that protects your money, your investment, and your peace of mind.

Remember: it’s not just about the monthly payment. Consider the loan terms, insurance coverage, maintenance costs, and emerging trends like EV incentives or usage-based insurance. Doing your homework upfront can save you headaches and even thousands of dollars over time.

May be you like it:

Best Day Trading Setup – Simple Strategies That Work

Business Finance Definition Made Easy for Understanding Info