Introduction

You’ve finally found the car you’ve been eyeing. It drives well, looks great, and fits your needs perfectly. But then comes the big question: should I pay cash or finance a car?

This isn’t just about money—it’s about your comfort, your savings, and how your finances will feel months down the road. Paying cash can give instant ownership and peace of mind, but it may drain your emergency fund. Financing keeps cash in your pocket, but adds monthly obligations and interest.

In this guide, we’ll break down the benefits, risks, and practical strategies for both options, helping you make a choice that fits your lifestyle and keeps your wallet—and your stress levels—under control.

Table of Contents

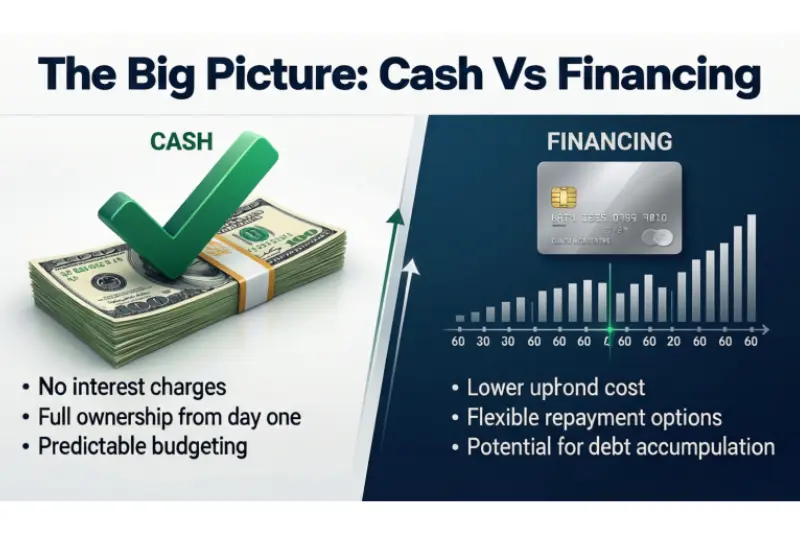

The Big Picture: Cash vs Financing

At its core, the question of should I pay cash or finance a car comes down to one simple difference: paying everything upfront versus spreading the cost over time.

Paying cash means the car is entirely yours from day one. You hand over the money, drive off, and never worry about monthly bills again. Financing, on the other hand, lets you keep most of your cash while paying smaller chunks each month, often with interest. That can feel safer in the short term but extends your financial commitment into the future.

Neither choice is inherently “better.” Paying cash isn’t automatically smarter, and financing isn’t automatically risky. The real difference lies in how each option interacts with your lifestyle, savings, and peace of mind. Some people sleep better knowing the car is fully paid off. Others feel more comfortable keeping a cushion of cash in the bank, even if it means owing a lender for a few years.

Ultimately, this decision isn’t just about money-it’s about the stress you carry, the flexibility you need, and how confident you feel managing your finances while still enjoying your new car.

May be you like it:

How Long Does It Take to Learn Day Trading Effectively?

Boost Your Career with an Online Accounting Diploma

Smart Strategies for Generational Wealth Management

What Is a Smart Investment – Simple Guide for Beginners

Paying Cash: Benefits

There’s something undeniably satisfying about handing over the full amount and walking away debt-free. When you pay cash for a car, you own it outright from day one. No monthly payments, no surprises, and no lender checking in. For many people, that feeling alone is worth the upfront cost.

Another big advantage is avoiding interest and long-term debt. Even a “low” auto loan interest rate can add up to hundreds-or thousands-over the life of the loan. Paying cash eliminates that entirely, so the price you see is the price you actually pay.

Cash buyers also often get better negotiating power, especially when buying used cars. Sellers love quick, hassle-free transactions, and knowing you can pay immediately can give you leverage to secure a better deal.

Finally, there’s the emotional comfort of owning your car outright. For some, simply knowing there’s no monthly obligation hanging over their head brings peace of mind. You can drive, trade, or sell your car without any lender approval, which is a small but meaningful freedom many buyers value.

Paying Cash: Drawbacks

Paying cash isn’t always as carefree as it seems. The most obvious downside is the large upfront cost, which can seriously shrink your emergency savings. Handing over tens of thousands of dollars at once can feel empowering-but if life throws an unexpected expense your way, suddenly that freedom feels risky.

There’s also the opportunity cost to consider. That cash could be invested, earning interest or returns elsewhere. By using it all on a car, you might miss out on growing your money over time.

Another drawback is reduced financial flexibility. If something unexpected happens-like a home repair, medical bill, or job delay-you might find yourself short on liquid funds. I’ve seen friends proudly pay cash, then quietly stress when a minor emergency popped up. One even had to dip into a credit card just to cover routine repairs, all because their savings were tied up in a car that was “fully theirs.”

Paying cash gives you ownership, but it also comes with the hidden cost of less breathing room for life’s surprises.

Financing a Car: Benefits

Financing a car can feel like a safety net for your finances. One of the biggest advantages is that it keeps cash available. Instead of handing over a large sum upfront, you can keep money in your savings account for emergencies, unexpected expenses, or even opportunities like investments or a side project.

Another benefit is predictable monthly payments. Knowing exactly what you’ll pay each month makes budgeting easier and can reduce stress. For someone with a steady income, this predictability is often more valuable than outright ownership.

Sometimes, financing comes with low interest rates or manufacturer incentives, especially on new cars. These deals can make borrowing surprisingly affordable, even cheaper than some buyers expect.

Finally, financing responsibly can help build your credit. Making on-time payments shows lenders you can handle debt, which can improve your credit score and open doors for future loans or mortgages.

In short, financing offers flexibility, financial planning advantages, and even long-term benefits if managed wisely.

Financing a Car: Risks

Financing a car isn’t automatically bad, but it comes with some hidden costs and potential pitfalls. First off, interest increases the total price. Even a seemingly low rate can add up to thousands of extra dollars over the life of the loan. That’s money you’ll never get back.

Monthly payments can also mask the real cost of the car. A $400 monthly payment sounds reasonable until you realize it stretches over five or six years, turning a $25,000 car into a much more expensive long-term commitment. This can tempt buyers to purchase a pricier car than they initially intended.

Another common risk is owing more than the car is worth, especially in the first few years. Cars depreciate quickly, and early on, your loan balance may exceed the car’s market value. If you need to sell or trade the car during this period, you could face a financial hit.

Finally, there’s the emotional weight of debt. Some people feel anxious or restricted knowing they owe money, even if the payments are manageable. That mental load can turn what should be an exciting purchase into a source of stress.

Financing works well for many, but it’s important to be aware of these risks before signing on the dotted line.

Key Questions to Ask Yourself Before Deciding

When it comes to should I pay cash or finance a car, there’s no universal answer. The right choice depends on your life, finances, and comfort level. Asking yourself a few honest questions can make the decision much clearer.

- Am I comfortable with my savings after paying cash?

If dropping a large sum leaves you anxious or with no safety net, paying cash might not be the best move. - Can I handle monthly payments without stress?

Even if the math works out, emotional comfort matters. Some people sleep better without debt, while others feel fine with structured payments. - Is my income stable?

A steady income makes financing much easier. If your earnings fluctuate, large monthly payments could become stressful. - Would a mixed approach make sense?

Sometimes a combination-like a large down payment plus a short-term loan-offers the best of both worlds. - How does my personal attitude toward debt affect my choice?

Your comfort with borrowing plays a huge role. If debt gives you anxiety, even a low-interest loan might not be worth it.

Answering these questions honestly will guide you toward a choice that feels practical, manageable, and right for your unique situation.

The Balanced Option Most Buyers Overlook

Not everyone has to choose between all-cash or full financing. For many buyers, the middle-ground approach-making a large down payment and financing the rest over a short term-offers the best of both worlds.

This strategy reduces interest costs because you’re borrowing less, while still protecting your cash reserves for emergencies or unexpected expenses. At the same time, you avoid being tied to long-term payments, which keeps your financial flexibility intact.

Think of it as a compromise that doesn’t feel like a compromise. You get the satisfaction of owning a significant portion of the car upfront, the security of keeping some savings intact, and the peace of mind that comes with short-term, manageable payments.

For many people, this approach ends up being the most practical and stress-free solution, combining financial responsibility with lifestyle flexibility.

New vs Used Cars: Payment Implications

Whether you’re buying a new or used car can significantly affect whether paying cash or financing makes more sense.

Used cars often favor cash buyers. Prices are lower, and sellers usually appreciate fast, hassle-free transactions. Handing over cash can even give you leverage to negotiate a better deal. For buyers who prefer simplicity and want to avoid interest on a smaller purchase, paying cash can be ideal.

New cars, on the other hand, can make financing more appealing. Manufacturers sometimes offer low or even 0% APR deals, rebates, or incentives that make borrowing surprisingly affordable. In these cases, financing might cost less than paying cash outright-especially if you want to keep some savings intact.

That said, proceed with caution. Dealerships are skilled at making offers look “too good to be true,” especially under pressure. Take your time, read the fine print, and run the numbers yourself. A shiny monthly payment doesn’t always mean a smart financial decision.

Understanding the differences between new and used cars can help you choose a payment method that fits your budget, lifestyle, and long-term peace of mind.

Common Mistakes to Avoid

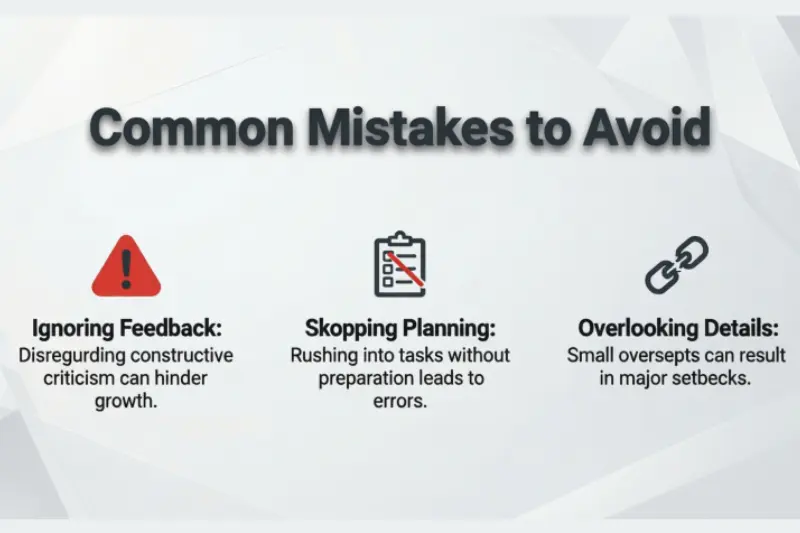

Even with all the information in front of you, it’s easy to fall into common traps when deciding should I pay cash or finance a car. Here are the mistakes buyers often regret:

- Choosing based only on monthly payment

A low monthly payment can be tempting, but it doesn’t show the full picture. Stretching a loan over many years may make the car seem affordable now, but it increases total interest paid and ties you down longer than necessary. - Emptying savings just to avoid debt

Paying cash feels clean and satisfying-but draining your emergency fund can create stress and risk when unexpected expenses arise. A car shouldn’t leave you financially exposed. - Taking excessively long loans

Some buyers extend loans for 6–7 years to reduce monthly payments. While it seems smart at first, long-term loans increase interest and often leave you owing more than the car’s value early on. - Ignoring total interest cost

It’s easy to focus on the monthly number, but long-term interest can quietly add thousands to the car’s price. Always calculate the full cost before deciding. - Rushing the decision due to urgency or sales pressure

“Deal ends today!” or “This car won’t last!” are classic tactics. Taking your time ensures you make a choice that fits your life, not someone else’s sales target.

Avoiding these mistakes keeps the purchase from becoming a source of stress or regret, and helps ensure your car adds value and convenience to your life rather than financial strain.

May be you like it:

Free Trading Webinar: Learn Smart Market Strategies

Certificate in Business Management Online: Your Career Boost

Smart Generational Wealth Planning for Lasting Legacy

Top Personal Investment Company Tips for Smart Investors

FAQs

Should I pay cash for a car if I have the money?

Yes, if doing so won’t drain your savings and you want debt-free ownership.

Is financing always more expensive than paying cash?

Not necessarily—low interest rates and incentives can make financing cost-effective.

Can I negotiate better if I pay cash?

Often, yes. Sellers love quick, hassle-free cash transactions, especially on used cars.

Will financing hurt my credit?

No, if you make on-time payments. In fact, it can improve your credit score.

How do I know if I can handle monthly payments?

Review your budget, account for emergencies, and ensure payments don’t stress your monthly finances.

Is paying cash risky?

It can be if it leaves you with too little savings for emergencies or unexpected expenses.

Should I always take the shortest loan term possible?

Shorter terms reduce interest, but make sure the monthly payment fits comfortably in your budget.

Is it smarter to buy new or used with cash?

Used cars often favor cash due to lower prices, while new cars sometimes make financing attractive through incentives.

Can I combine both options?

Absolutely—a large down payment with a short-term loan often balances flexibility, interest savings, and peace of mind.

What’s the biggest mistake buyers make?

Choosing only based on monthly payments, without considering total cost, savings, or stress level.

Final Thoughts

So, should I pay cash or finance a car? The answer isn’t universal-it depends on your savings, your income, and how comfortable you are with debt.

Pay cash if you can do it without draining your emergency fund and you value simplicity. Finance if the rate is reasonable, your income is steady, and keeping cash on hand matters more than being debt-free.

Remember, the smartest choice isn’t the one that looks best on paper-it’s the one that still feels manageable months down the road. Picture yourself in six months: bills paid, savings intact, and still enjoying your car without stress. If your decision leads to that, you’ve made the right choice.

Buying a car is exciting, but the best decisions are the ones that quietly support your life. Choose a path that keeps both your wallet and your peace of mind intact.

May be you like it:

Stock Market for Beginners PDF – Your Simple Starter Guide

Top MBA Certificate Programs Online for Career Growth